In regression analysis, the variance inflation factor (VIF) is a measure of the degree of multicollinearity of one regressor with the other regressors.

![]()

Table of contents

Multicollinearity arises when a regressor is very similar to a linear combination of other regressors.

Multicollinearity has the effect of markedly increasing the variance of regression coefficient estimates. Therefore, we usually try to avoid it as much as possible.

To detect and measure multicollinearity, we use the so-called variance inflation factors.

Consider the linear

regression![]() where:

where:

![]() is the dependent variable;

is the dependent variable;

![]() are

are

![]() regressors;

regressors;

![]() are

are

![]() regression coefficients;

regression coefficients;

![]() is the error term;

is the error term;

the observations are indexed by

![]() .

.

The linear regression can be written in matrix form

as:![]() where:

where:

![]() and

and

![]() are

are

![]() vectors;

vectors;

![]() is an

is an

![]() matrix;

matrix;

![]() is a

is a

![]() vector.

vector.

If the design matrix

![]() has full rank, then we can

compute the ordinary least squares (OLS) estimator of the vector of regression

coefficients

has full rank, then we can

compute the ordinary least squares (OLS) estimator of the vector of regression

coefficients

![]() as

follows:

as

follows:![]()

Under certain assumptions (see, e.g., the lecture on the

Gauss-Markov

theorem), the covariance matrix of the OLS estimator

is![]()

Therefore, the variance of the OLS estimator of a single coefficient

is![]() where

where

![]() is the

is the

![]() -th

entry on the main diagonal of

-th

entry on the main diagonal of

![]() .

.

If the

![]() -th

regressor has zero mean, we can write the variance of its estimated

coefficient

as

-th

regressor has zero mean, we can write the variance of its estimated

coefficient

as![[eq10]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where

where

![]() is the

R

squared obtained by regressing the

is the

R

squared obtained by regressing the

![]() -th

regressor on all the other regressors.

-th

regressor on all the other regressors.

Without loss of generality, suppose that

![]() (otherwise, change the order of the regressors). We can write the design

matrix

(otherwise, change the order of the regressors). We can write the design

matrix

![]() as a block

matrix:

as a block

matrix:![]() where

where

![]() is the first column of

is the first column of

![]() and the block

and the block

![]() contains all the other columns. Then, we

haveWe

use Schur complements, and in

particular the

formula

contains all the other columns. Then, we

haveWe

use Schur complements, and in

particular the

formula![[eq13]](/images/variance-inflation-factor__36.png) to

write the first entry of the inverse of

to

write the first entry of the inverse of

![]() as:

as:![[eq14]](/images/variance-inflation-factor__38.png) As

proved in the lecture on

partitioned

regressions, the matrix

As

proved in the lecture on

partitioned

regressions, the matrix

![]() is idempotent and symmetric; moreover, when it is post-multiplied by

is idempotent and symmetric; moreover, when it is post-multiplied by

![]() ,

it gives as a result the residuals of a regression of

,

it gives as a result the residuals of a regression of

![]() on

on

![]() .

The vector of these residuals is denoted

by

.

The vector of these residuals is denoted

by![]() Therefore,

Therefore,

![[eq17]](/images/variance-inflation-factor__44.png) If

If

![]() has zero mean, the R squared of the regression of

has zero mean, the R squared of the regression of

![]() on

on

![]() is

Note

that this formula for the R squared is correct only if

is

Note

that this formula for the R squared is correct only if

![]() has zero mean. Then, we can

write

has zero mean. Then, we can

write![]() Therefore,and

Therefore,and

If the

![]() -th

regressor is orthogonal to all the other regressors, we can write the

variance of its estimated coefficient

as

-th

regressor is orthogonal to all the other regressors, we can write the

variance of its estimated coefficient

as![]()

As in the previous proof, we assume without

loss of generality that

![]() .

In that proof, we have demonstrated

that

.

In that proof, we have demonstrated

that![[eq23]](/images/variance-inflation-factor__56.png) If

If

![]() is orthogonal to all the columns in

is orthogonal to all the columns in

![]() ,

then

,

then![]() Therefore,

Therefore,

![[eq25]](/images/variance-inflation-factor__60.png)

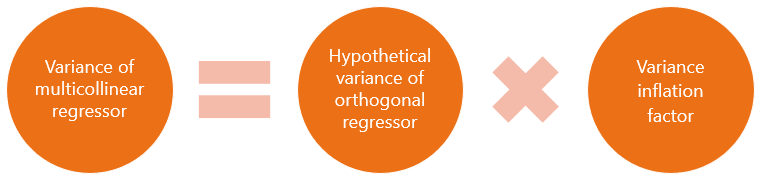

Thus, the variance of

![]() is the product of two terms:

is the product of two terms:

the variance that

![]() would have if the

would have if the

![]() -th

regressor were orthogonal to all the other regressors;

-th

regressor were orthogonal to all the other regressors;

the term

![]() ,

where

,

where

![]() is the R squared in a regression of the

is the R squared in a regression of the

![]() -th

regressor on all the other regressors.

-th

regressor on all the other regressors.

The second term is called the variance inflation factor

because it inflates the variance of

![]() with respect to the base case of orthogonality.

with respect to the base case of orthogonality.

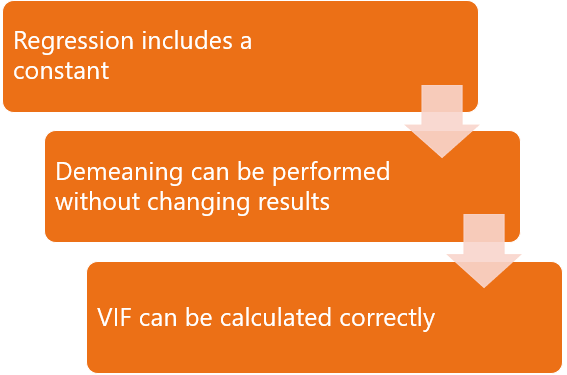

In order to derive the VIF, we have made the important assumption that the

![]() -th

regressor has zero mean.

-th

regressor has zero mean.

If this assumption is not met, then it is incorrect to compute the

VIF as

because

the latter is no longer a factor in the formula that relates the actual

variance of

![]() to its hypothetical variance under the assumption of orthogonality.

to its hypothetical variance under the assumption of orthogonality.

One way to make sure that the zero-mean assumption is met is to run a demeaned regression: before computing the OLS coefficient estimates, we demean all the variables.

As explained in the lecture on partitioned regression, demeaning does not change the coefficient estimates, provided that the regression includes a constant.

Note that a demeaned regression is a special case of a standardized regression. Therefore, we can run a standardized regression before computing variance inflation factors.

We have explained above that the VIF provides a comparison between the actual variance of a coefficient estimator and its hypothetical variance (under the assumption of orthogonality).

By definition, the

![]() -th

regressor is orthogonal to all the other regressors if and only

if

-th

regressor is orthogonal to all the other regressors if and only

if![]() for

all

for

all

![]() .

.

If the

![]() -th

regressor has zero mean, then the orthogonality condition is

equivalent to saying that the

-th

regressor has zero mean, then the orthogonality condition is

equivalent to saying that the

![]() -th

regressor is

uncorrelated

with all the other regressors.

-th

regressor is

uncorrelated

with all the other regressors.

Denote the sample means of

![]() and

and

![]() by

by

![]() and

and

![]() .

We assume that

.

We assume that

![]() .

Then, the sample covariance between

.

Then, the sample covariance between

![]() and

and

![]() is

Therefore,

is

Therefore,

![]() and

and

![]() are uncorrelated.

are uncorrelated.

This is why, if the

![]() -th

regressor has zero mean, the VIF provides a comparison between:

-th

regressor has zero mean, the VIF provides a comparison between:

the actual variance of a coefficient estimator;

the variance that the estimator would have if the corresponding variable were uncorrelated with all the other regressors.

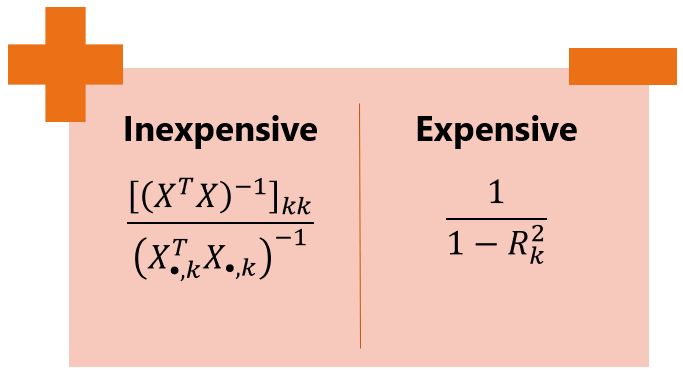

We usually compute the VIF for all the regressors. If there are many

regressors and the sample size is large, computing the VIF

ascan

be quite burdensome because we need to run many large regressions (one for

each

![]() )

in order to compute

)

in order to compute

![]() different R squareds.

different R squareds.

A better alternative is to use the equivalent

formulawhich

can be easily derived from the formulae given above.

We have proved

thatwhich

implies

that

When we use the latter formula, we compute

![]() only once. Then, we use its

only once. Then, we use its

![]() diagonal entries to compute the

diagonal entries to compute the

![]() VIFs.

VIFs.

The numbers

![]() in the denominator are easy to calculate because each of them is the

reciprocal of the inner product of a vector with itself.

in the denominator are easy to calculate because each of them is the

reciprocal of the inner product of a vector with itself.

Here is the final recipe for computing the variance inflation factors:

Make sure that your regression includes a constant (otherwise this recipe cannot be used).

Demean all the variables and drop the constant.

Compute

![]() .

.

For each

![]() compute

compute

![]() .

.

The VIF for the

![]() -th

regressor

is

-th

regressor

is

The VIF is equal to 1 if the regressor is uncorrelated with the other regressors, and greater than 1 in case of non-zero correlation.

The greater the VIF, the higher the degree of multicollinearity.

In the limit, when multicollinearity is perfect (i.e., the regressor is equal to a linear combination of other regressors), the VIF tends to infinity.

There is no precise rule for deciding when a VIF is too high (O'Brien 2007), but values above 10 are often considered a strong hint that trying to reduce the multicollinearity of the regression might be worthwhile.

In the lecture on Multicollinearity, we discuss in more detail the interpretation of the variance inflation factor, and we explain how to deal with multicollinearity.

O'Brien, R. (2007) A Caution Regarding Rules of Thumb for Variance Inflation Factors, Quality & Quantity, 41, 673-690.

Previous entry: Variance formula

Please cite as:

Taboga, Marco (2021). "Variance inflation factor", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/glossary/variance-inflation-factor.

Most of the learning materials found on this website are now available in a traditional textbook format.