The Poisson distribution is a discrete probability distribution used to model the number of occurrences of a random event.

![]()

Suppose that an event can occur several times within a given unit of time.

When the total number of occurrences of the event is unknown, we can think of it as a random variable.

This random variable has a Poisson distribution if the time elapsed between two successive occurrences of the event:

has an exponential distribution;

it is independent of previous occurrences.

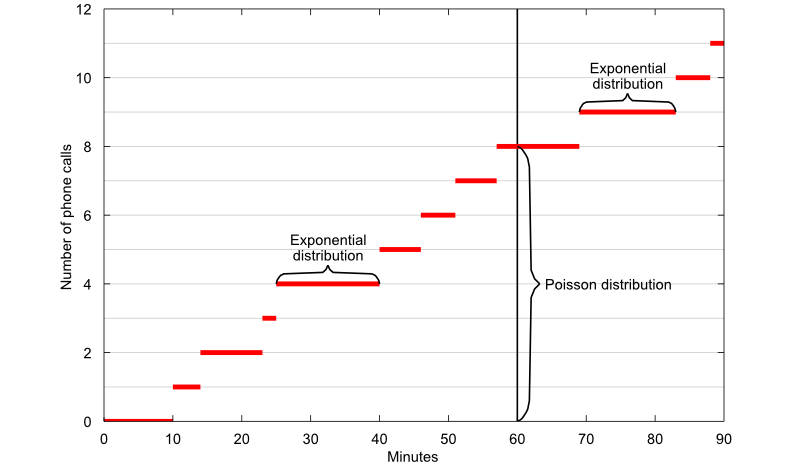

A classical example of a random variable having a Poisson distribution is the number of phone calls received by a call center.

If the time elapsed between two successive phone calls has an exponential distribution and it is independent of the time of arrival of the previous calls, then the total number of calls received in one hour has a Poisson distribution.

The concept is illustrated by the plot above, where the number of phone calls received is plotted as a function of time:

the graph of the function makes an upward jump each time a phone call arrives;

the time elapsed between two successive phone calls is equal to the length of each horizontal segment and it has an exponential distribution;

the number of calls received in 60 minutes is equal to the length of the segment highlighted by the vertical curly brace and it has a Poisson distribution.

A Poisson random variable is characterized as follows.

Definition

Let

![]() be a discrete random

variable. Let its

support be the set

of non-negative integer

numbers:

be a discrete random

variable. Let its

support be the set

of non-negative integer

numbers:![]() Let

Let

![]() .

We say that

.

We say that

![]() has a Poisson distribution with parameter

has a Poisson distribution with parameter

![]() if its probability mass

function

is

if its probability mass

function

is![[eq3]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where

where

![]() is the factorial of

is the factorial of

![]() .

.

The relation between the Poisson distribution and the exponential distribution is summarized by the following proposition.

Proposition

The number of occurrences of an event within a unit of time has a Poisson

distribution with parameter

![]() if the time elapsed between two successive occurrences of the event has an

exponential distribution with parameter

if the time elapsed between two successive occurrences of the event has an

exponential distribution with parameter

![]() and it is independent of previous occurrences.

and it is independent of previous occurrences.

Denote by

![]() the number of occurrences of the event and

by

the number of occurrences of the event and

by![[eq4]](/images/Poisson-distribution__12.png) Note

that there are at least

Note

that there are at least

![]() occurrences of the event (i.e.,

occurrences of the event (i.e.,

![]() )

within a unit of time if and only if the sum of the times elapsed between the

)

within a unit of time if and only if the sum of the times elapsed between the

![]() occurrences is less than one unit of time. In other words, the events

occurrences is less than one unit of time. In other words, the events

![]() and

and

![]() coincide.

Therefore,

coincide.

Therefore,![]() for

any

for

any

![]() .

Thus, the distribution of

.

Thus, the distribution of

![]() can be derived from the distribution of the waiting times

can be derived from the distribution of the waiting times

![]() .

We are going to prove that the assumption that the waiting times are

exponential implies that

.

We are going to prove that the assumption that the waiting times are

exponential implies that

![]() has a Poisson distribution. Denote by

has a Poisson distribution. Denote by

![]() the sum of waiting

times:

the sum of waiting

times:![]() Since

the sum of independent exponential random

variables with common parameter

Since

the sum of independent exponential random

variables with common parameter

![]() is a Gamma random variable with parameters

is a Gamma random variable with parameters

![]() and

and

![]() ,

then

,

then

![]() is a Gamma random variable with parameters

is a Gamma random variable with parameters

![]() and

and

![]() ,

i.e., its probability

density function

iswhere

and

the last equality stems from the fact that we are considering only integer

values of

,

i.e., its probability

density function

iswhere

and

the last equality stems from the fact that we are considering only integer

values of

![]() .

We need to integrate the density function to compute the probability that

.

We need to integrate the density function to compute the probability that

![]() is less than

is less than

![]() :The

last integral can be computed integrating by parts

:The

last integral can be computed integrating by parts

![]() times:

times:![[eq13]](/images/Poisson-distribution__38.png) Multiplying

by

Multiplying

by

![]() ,

we

obtainThus,

we have

obtained

,

we

obtainThus,

we have

obtained![[eq15]](/images/Poisson-distribution__41.png) But

this is exactly what we get when

But

this is exactly what we get when

![]() has a Poisson

distribution:

has a Poisson

distribution:

The expected value of a Poisson random variable

![]() is

is![]()

It

can be derived as

follows:![[eq18]](/images/Poisson-distribution__46.png)

The variance of a Poisson random variable

![]() is

is![]()

It

can be derived thanks to the usual

variance formula

(![]() ):

):![[eq21]](/images/Poisson-distribution__50.png)

The moment generating function of a Poisson

random variable

![]() is defined for any

is defined for any

![]() :

:![]()

By

using the definition of moment generating function, we

getwhereis

the usual Taylor series expansion of the exponential function. Furthermore,

since the series converges for any value of

![]() ,

the moment generating function of a Poisson random variable exists for any

,

the moment generating function of a Poisson random variable exists for any

![]() .

.

The characteristic function of a Poisson random

variable

![]() is

is![]()

By

using the definition of characteristic function, we

obtainwhereis

the usual Taylor series expansion of the exponential function (note that the

series converges for any value of

![]() ).

).

The distribution function

of a Poisson random variable

![]() iswhere

iswhere

![]() is

the floor of

is

the floor of

![]() ,

i.e. the largest integer not greater than

,

i.e. the largest integer not greater than

![]() .

.

By using the definition of distribution

function, we

get![[eq30]](/images/Poisson-distribution__68.png)

Values of

![]() are usually computed by computer algorithms. For example, the MATLAB command:

are usually computed by computer algorithms. For example, the MATLAB command:

poisscdf(x,lambda)

returns the value of the distribution function at the point

x when the parameter of the distribution is equal to

lambda.

Below you can find some exercises with explained solutions.

The time elapsed between the arrival of a customer at a shop and the arrival of the next customer has an exponential distribution with expected value equal to 15 minutes. Furthermore, it is independent of previous arrivals.

What is the probability that more than 6 customers arrive at the shop during the next hour?

If a random variable has an exponential

distribution with parameter

![]() ,

then its expected value is equal to

,

then its expected value is equal to

![]() .

Here

.

Here![]() Therefore,

Therefore,

![]() .

If inter-arrival times are independent exponential random variables with

parameter

.

If inter-arrival times are independent exponential random variables with

parameter

![]() ,

then the number of arrivals during a unit of time has a Poisson distribution

with parameter

,

then the number of arrivals during a unit of time has a Poisson distribution

with parameter

![]() .

Thus, the number of customers that will arrive at the shop during the next

hour (denote it by

.

Thus, the number of customers that will arrive at the shop during the next

hour (denote it by

![]() )

is a Poisson random variable with parameter

)

is a Poisson random variable with parameter

![]() .

The probability that more than 6 customers arrive at the shop during the next

hour

is

.

The probability that more than 6 customers arrive at the shop during the next

hour

is![[eq33]](/images/Poisson-distribution__78.png) and

the value of

and

the value of

![]() can be calculated with a computer algorithm, for example with the MATLAB

command

can be calculated with a computer algorithm, for example with the MATLAB

command![]()

At a call center, the time elapsed between the arrival of a phone call and the arrival of the next phone call has an exponential distribution with expected value equal to 15 seconds. Furthermore, it is independent of previous arrivals.

What is the probability that less than 50 phone calls arrive during the next 15 minutes?

If a random variable has an exponential

distribution with parameter

![]() ,

then its expected value is equal to

,

then its expected value is equal to

![]() .

Here

.

Here![]() where,

in the last equality, we have taken 15 minutes as the unit of time. Therefore,

where,

in the last equality, we have taken 15 minutes as the unit of time. Therefore,

![]() .

If inter-arrival times are independent exponential random variables with

parameter

.

If inter-arrival times are independent exponential random variables with

parameter

![]() ,

then the number of arrivals during a unit of time has a Poisson distribution

with parameter

,

then the number of arrivals during a unit of time has a Poisson distribution

with parameter

![]() .

Thus, the number of phone calls that will arrive during the next 15 minutes

(denote it by

.

Thus, the number of phone calls that will arrive during the next 15 minutes

(denote it by

![]() )

is a Poisson random variable with parameter

)

is a Poisson random variable with parameter

![]() .

The probability that less than 50 phone calls arrive during the next 15

minutes

is

.

The probability that less than 50 phone calls arrive during the next 15

minutes

is![[eq37]](/images/Poisson-distribution__89.png) and

the value of

and

the value of

![]() can be calculated with a computer algorithm, for example with the MATLAB

command

can be calculated with a computer algorithm, for example with the MATLAB

command

poisscdf(49,60)

Please cite as:

Taboga, Marco (2021). "Poisson distribution", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/probability-distributions/Poisson-distribution.

Most of the learning materials found on this website are now available in a traditional textbook format.