What is the probability that the realization of a random variable will be less than or equal to a certain threshold value?

The distribution function of a random variable allows us to answer exactly this question.

Its value at a given point is equal to the probability of observing a realization of the random variable below that point or equal to that point.

![]()

The distribution function is also often called cumulative distribution function (abbreviated as cdf).

The following is a formal definition.

Definition

If

![]() is a random variable, its distribution function is a function

is a random variable, its distribution function is a function

![]() such

that

such

that![]() where

where

![]() is the probability

that

is the probability

that

![]() is less than or equal to

is less than or equal to

![]() .

.

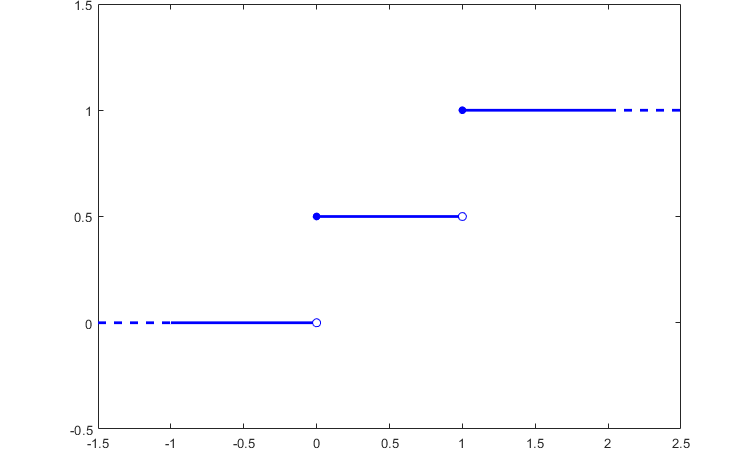

Suppose that a random variable can take only two values (0 and 1), each with probability 1/2.

Its distribution function

is![[eq4]](/images/distribution-function__7.png)

Here is a plot of the function.

Every distribution function enjoys the following four properties:

Increasing.

![]() is increasing, i.e.,

is increasing, i.e.,

![]()

Right-continuous.

![]() is right-continuous,

i.e.,

is right-continuous,

i.e.,![[eq8]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) for

any

for

any

![]() ;

;

Limit at minus infinity.

![]() satisfies

satisfies

![]()

Limit at plus infinity.

![]() satisfies

satisfies

![]()

Concise proofs of these properties can be found here and in Williams (1991).

Any distribution function enjoys the four properties above.

Moreover, for any given function enjoying these four properties, it is possible to define a random variable that has the given function as its distribution function (for a proof, see Williams 1991, Sec. 3.11).

The practical consequence of this fact is that, when we need to check whether a given function is a proper distribution function, we just need to verify that it satisfies the four properties above.

When the random variable

![]() is discrete, the cdf can be

derived

aswhere:

is discrete, the cdf can be

derived

aswhere:

![]() is the support of

is the support of

![]() ;

;

![]() is the probability mass

function of

is the probability mass

function of

![]() .

.

This can be quickly done with a table.

Suppose that the probability mass function of

![]() is

is![[eq15]](/images/distribution-function__24.png)

Then, we can set up a table that has three rows.

In the first row, we write the possible values of

![]() ,

sorted from smallest to largest.

,

sorted from smallest to largest.

In the second row, we write the probabilities of the single values.

The third row contains the values of the cdf.

The leftmost cell in the third row is equal to the cell immediately above.

Then, we go from left to right and the value in each cell is set equal to the sum of:

the probability in the cell immediately to the left;

the probability in the cell immediately above.

![[eq16]](/images/distribution-function__26.png)

Thus, the distribution function

is![[eq17]](/images/distribution-function__27.png)

When the random variable is

continuous, its

cdf can be computed

as![]() where

where

![]() is the probability density

function of

is the probability density

function of

![]() .

.

The simplest example is probably the cdf of the uniform distribution.

The probability density function of a random variable having uniform

distribution on the interval

![]() is

is![]() where

where

![]() is an indicator function that takes value 1 on the interval

is an indicator function that takes value 1 on the interval

![]() and value 0 everywhere else.

and value 0 everywhere else.

There are three cases:

if

![]() ,

then

,

then![]()

if

![]() ,

then

,

then![]()

if

![]() ,

then

,

then![]()

Therefore, the cdf

is![[eq26]](/images/distribution-function__41.png)

More details about the distribution function can be found in the lecture on Random variables.

Williams, D., 1991. Probability with martingales. Cambridge university press.

Previous entry: Discrete random vector

Next entry: Estimator

Please cite as:

Taboga, Marco (2021). "Distribution function", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/glossary/distribution-function.

Most of the learning materials found on this website are now available in a traditional textbook format.